Midyear Hydration Break

With the recent conclusion of the FIFA World Cup, one of the passionately debated topics was the merit of the “hydration break”, which took place midway through each half of every match. The soccer purists despised them, while the advertisers rejoiced.

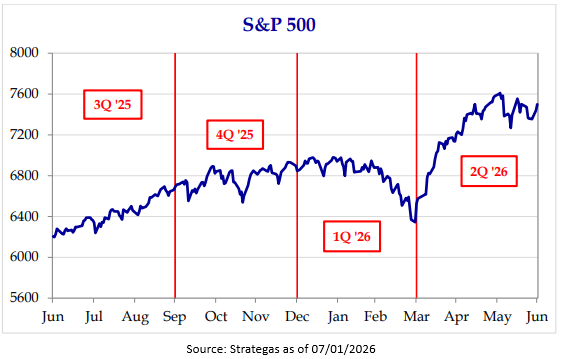

For teams surging with their opponents on the ropes, the hydration break meant potentially losing momentum with the stoppage of play. Markets are not dissimilar in that momentum is a powerful factor that draws investors of all types into the market. The market itself surged in the second quarter of 2026 as the S&P 500 returned +15.2%1. This represented the best quarterly return since 2020 for the S&P 5002.

Midterm election years historically are the most volatile years for the equity market during the four-year presidential cycle3. Furthermore, the second quarter of a mid-term year is typically the worst quarter in the entire four-year cycle of a president’s term3.

Most investors might assume that for such a robust recovery given the historical precedent of weakness, the conflict with Iran found a resolution – but it did not. In fact, in recent weeks, tension has been rising as the MOU (memorandum of understanding) was dissolved. Despite this, the S&P 500 had its best return in the second quarter of a midterm election year since 1936 – when a new Ford Model 68 sold for $5103,4.

The sentiment exiting the first quarter reminded me of one of my favorite stories from the late Art Cashin, who was famous for his career at UBS and CNBC. He was a young man in the 1960’s during the Cuban Missile Crisis. I’ll paraphrase, but on a rumor that Russia launched missiles the market sunk. Young Art frantically yelled to his mentor that he tried to sell the market. Art’s mentor told him when the missiles are flying, you buy5.

Being willing to buy at the most uncomfortable times may often yield some of the best returns. During the second quarter the market largely looked through the conflict with Iran expecting that in due time a resolution may be found. The backbone of the second quarter recovery was initially led by artificial intelligence (“AI”) stocks. Later as AI skepticism grew, investors rotated into other sectors, such as healthcare and financials.

Heading into the second half of the year, investor expectations have risen. Several factors have the potential to disrupt the markets’ momentum and are worth monitoring:

• Re-escalation of conflict with Iran. This may impact economic growth and inflation expectations.

• Higher interest rates. This would be a headwind for interest rate sensitive sectors (ex: housing).

• AI-related stocks have high expectations. If they disappoint, stock prices may re-price lower.

• Seasonality. Typically, the middle part of a midterm election year affords more modest returns.

• A new Federal Reserve Chairman, Kevin Warsh. Markets typically test new Fed Chairs.

Investors remain optimistic, so we’re taking a prudent posture in being vigilant as it relates to risk-taking and the price we pay for investments – both in equities and fixed income. The economy is in transition as AI has its fingerprints on the disruption, but also policy and deglobalization reshape how companies are approaching their businesses and supply chains. We view the skepticism and bubble talk around AI as healthy as investors remain discerning – unlike the Dot.com bubble.

We continue to balance remaining invested in companies where valuations have risen that we believe are primary beneficiaries of the AI capital expenditure cycle while allocating to new ideas. This prudence to not abandon diversification paid off in the second quarter as many of our best performing stocks were outside of technology. One example being Financials.

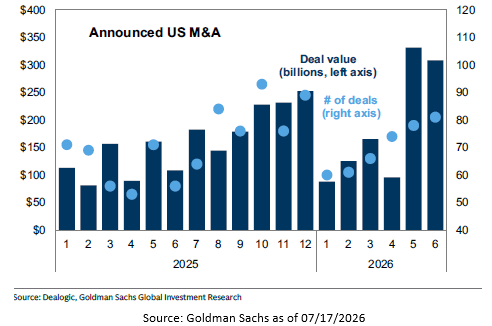

Financials carry the second-best forward profit margin estimates for the next twelve months after technology, and a forward price-to-earnings ratio that is the second lowest of the eleven sectors in the S&P 5007. This sector also has exposure to capital markets, where mergers and acquisition activity is accelerating8. Rising M&A activity is a sign of CEO confidence and bullish for the economy.

Our portfolio remains exposed to the hardware and infrastructure AI plays, such as semiconductors, wafer fabrication equipment (WFEs), power providers, and more. A continued focus is identifying second and third derivative beneficiaries where the potential benefits of AI adoption are long tailed.

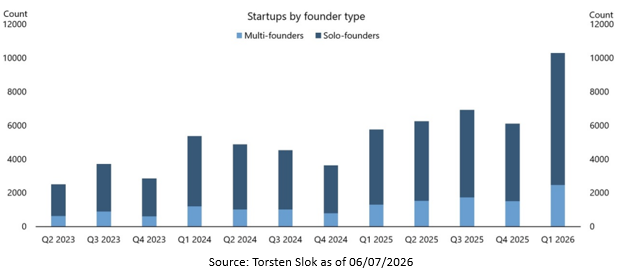

Deloitte, one of the largest consulting firms, found that 86% of enterprises surveyed expect their AI budgets to increase over the next three years, tripling on average9. AI is also leading to an explosion in business formation, especially by solo founders, and transforming how companies think about talent acquisition.

The market may have its own “hydration break” as it digests various developments in the months ahead after recent strength, but just like the FIFA World Cup games, the whistle will blow and the match will continue. We are approaching the second half of the year with cautious optimism and believe the outlook remains favorable for investors.

Thank you for your continued support and confidence in our team.

Bryce Goldbach, CFA®

Partner, Co-Chief Investment Officer

7/21/2026