Embracing the Unexpected – at Home and in Markets

As a dad of a busy toddler, you embrace chaos. Days are filled with darting from one activity to another – dinosaurs, monster trucks, library visits, and the park. A crucial lesson a parent learns is what you can’t control, no matter how well you plan.

Markets are similar. Each year investors position portfolios guided by history and expectations for the year ahead. Then as my college baseball coach would say “that’s why you play the game”. Reality often differs from expectations.

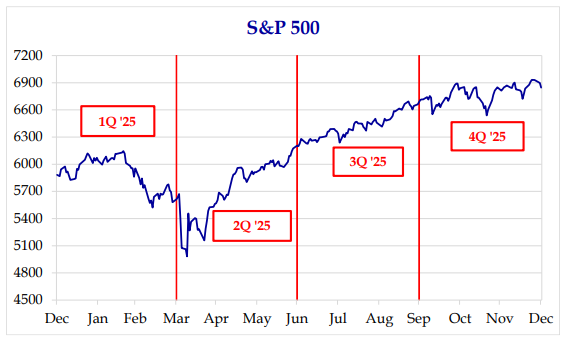

2025 was a year where narratives shifted faster than fundamentals. Headlines ranged from the Liberation Day tariffs that sparked panic selling in April to ongoing geopolitical tension across the globe. Despite this, it was a tremendous year for both equity and fixed income investors. The S&P 500 Index and the Bloomberg US Aggregate Bond Index returned +17.9% and +7.3%, respectively1.

Artificial intelligence remained the dominant theme in the market, but surprises emerged:

• First, international stocks outperformed domestic stocks aided by a weaker U.S. dollar. Having a global approach and investing in stocks domiciled outside the U.S. benefitted our portfolio in 20251.

• Second, the U.S. equity market broadened. Growth stocks continued to outperform, however, into year-end value stocks and small and mid-caps took the baton1.

• Lastly, only 2 of the Magnificent 7 stocks beat the S&P 500 (Nvidia, Google). The other 5 Magnificent 7 stocks underperformed - Microsoft, Apple, Meta, Amazon, and Tesla2.

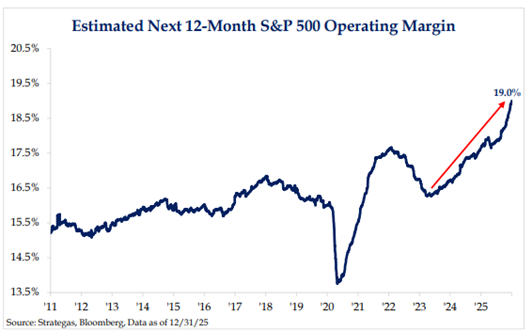

Corporate earnings continued to rise in 2025 led by an expansion of operating margins as companies experienced productivity gains spurred by investments in technology and artificial intelligence1. A productivity measure from the Bureau of Labor Statistics, which essentially looks at how efficiently the US economy is producing goods and services jumped to its highest level in two years during the third quarter of 20253.

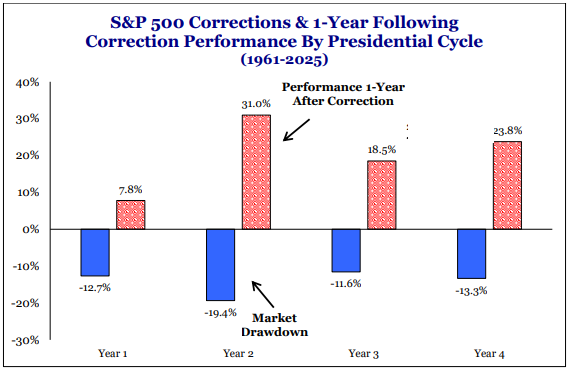

We enter 2026 with a favorable outlook but fully appreciate midterm years are choppy. The typical midterm year – or second year of a presidential cycle – is characterized by volatility and potential for sharper drawdowns than other years1. We view it as likely that equities will experience a sell off or correction in 2026 but are humble enough to acknowledge attempting to predict the timing is a fool’s game.

“Far more money has been lost by investors trying to anticipate corrections,

than lost in the corrections themselves4”

-Peter Lynch

Volatility often is uncomfortable, but it leads to fantastic opportunities to buy mispriced assets. Look no further than the Liberation Day sell-off of April 2025 previously referenced as a recent example. By constructing a durable, diversified portfolio, it enables our team to be on the offensive during these uncomfortable periods. Remaining invested is paramount, as while the drawdowns in midterm years may be larger than average, so are the subsequent recoveries1.

Despite anticipated volatility this year, there are numerous reasons for optimism:

• Corporate earnings are expected to grow above the long-term historical average5.

• The Federal Reserve is likely to further reduce interest rates.

• Trade war uncertainty remains but is fading.

• Artificial intelligence capital expenditures are robust.

• Falling oil prices allow for cheaper prices at the gas pump for consumers.

• The tax bill will be stimulative, including 100% bonus depreciation on equipment and factories6.

• The wealth effect, whereby as asset prices rise (home prices, stocks) people spend more.

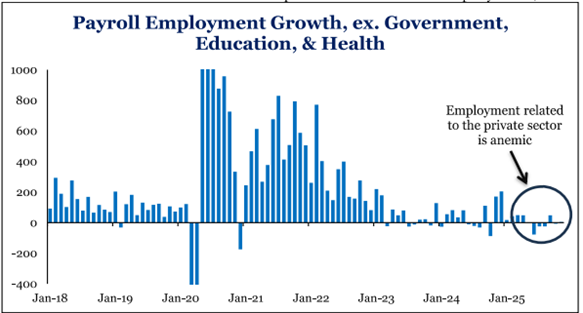

Investors are expecting roughly 0.50% of interest rate cuts for 20267. The health of the labor market will likely dictate if more interest rate cuts are necessary. Excluding healthcare, government, and education, job creation in the private sector is anemic, which is atypical during periods of strong economic growth1.

Given the scarcity of available labor, especially with changes to immigration policy, companies have been hoarding labor. Often characterized as a “slow to hire, slow to fire” environment. Companies are rapidly adopting AI, but it has yet to lead to an acceleration in layoffs. 2026 may be the year we see an acceleration of AI displacing workers.

A key debate heading into 2026 is whether artificial intelligence stocks are in a bubble, meaning asset prices are disconnected from economic reality. At any given time, certain pockets of the market may have characteristics of a bubble, such as unprofitable electric vehicle stocks in 2020-2021 as an example. Samantha McLemore, Founder of the investment firm Patient Capital, put it best – “Bubbles don’t typically peak when the world is on high alert” 8. We view it as healthy that investors remain vigilant, on high alert, and discerning.

Much like being a parent, as an investor, certain aspects of your environment are beyond your control. What is within your control is the amount of risk you take, the price you pay for an investment, and how you manage your emotions. While we expect increased volatility, we believe the backdrop is constructive for positive returns going forward.

Lastly, I’d be remiss without taking a moment to say thank you and express our gratitude to our clients. We are extremely blessed to serve you and appreciate your continued trust. We look forward to re-connecting with each of you in 2026.

Bryce Goldbach, CFA®

Portfolio Manager & Wealth Strategist

1/12/2026

Citations

[1] www.strategas.com “Quarterly Review in Charts Mon. Jan. 5, 2026.”

[2] www.ycharts.com “Roundhill Magnificent Seven ETF (MAGS) as of Jan 15, 2026.”

[3] www.barrons.com “Productivity is Rising even Without an AI Revolution as of 01/08/2026.”

[4] www.davisfunds.com “Don’t Try to Time the Market.” Peter Lynch.

[5] www.goldmansachs.com “The S&P 500 Is Expected to Rally 12% This Year as of 01/09/2026.”

[6] www.plantemoran.com “100% bonus depreciation returns with the One, Big, Beautiful Bill as of 07/21/2025.”

[7] www.cmegroup.com “CME FedWatch.”

[8] www.patientcapitalmanagement.com “Are We There Yet?”Samantha McLemore. 10/09/2025.

Disclosures

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Asio Capital makes no representation or warranty as to the accuracy or completeness of the information

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Asio Capital makes no representation or warranty as to the accuracy or completeness of the information

Disclosures

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Asio Capital makes no representation or warranty as to the accuracy or completeness of the information