Markets in the Crosscurrents

“Prediction is very difficult, especially if it’s about the future.”

-Niels Bohr1

It’s rarely what you expect that disrupts the market. Investors entered the year with optimism that economic momentum would potentially be bolstered by interest rate cuts, benefits of the One Big Beautiful Bill, and advances in productivity from artificial intelligence (AI).

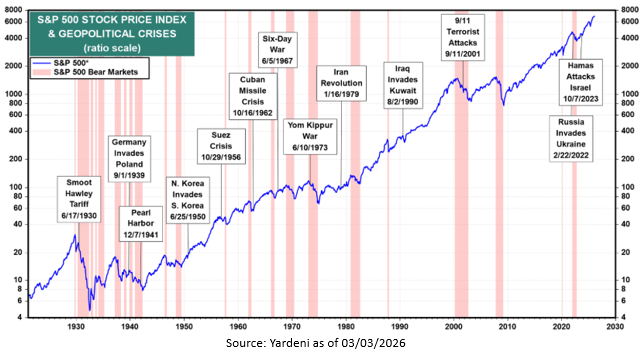

Early in the year the market digested a flurry of developments, such as contagion in private credit, the US invasion of Venezuela, and the AI apocalypse. It was not until late February when the US and Iran conflict began that investors turned more cautious.

Iran’s response was to essentially close the Strait of Hormuz, significantly impacting countries around the world who rely on the oil, natural gas, and other products that pass through this critical choke point. This led to rising commodity prices, higher yields, and renewed concerns about inflation.

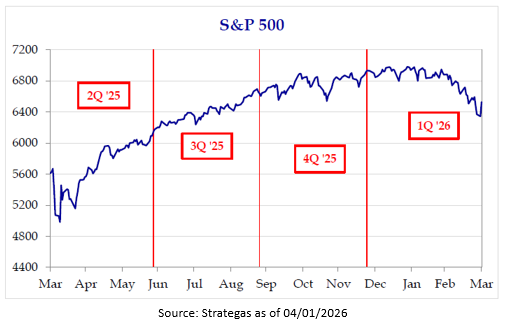

Equity markets responded accordingly. The S&P 500 declined 4.3% during the quarter2. March was where most of the damage took place as the S&P 500 Index had its worst March in a midterm year since 19423.

The pullback in equities was driven primarily by a decline in valuations rather than deterioration in fundamentals. Earnings expectations for the S&P 500 Index actually rose during the quarter2. Beneath the surface of the S&P 500 Index, dispersion of returns across individual stocks widened significantly as markets rapidly repriced risk and opportunity.

Today, the markets remain highly sensitive to developments in the Middle East – particularly the status of the Strait of Hormuz. The recent two-week ceasefire between the U.S. and Iran, though fragile, suggests a shared interest in avoiding prolonged escalation.

The duration of the conflict remains the key variable. A shorter, contained resolution would likely allow markets to refocus on underlying economic and corporate fundamentals. Prolonged disruption, however, could weigh on growth and confidence.

Periods like this often test discipline. Markets have reacted quickly to headlines, creating short-term volatility. For long-term investors, this environment has also created opportunity. We’ve used the recent volatility to take several deliberate actions across portfolios:

• Deploy capital where valuations have become attractive.

• Upgrade portfolio quality by emphasizing durable businesses.

• Harvest tax losses in applicable accounts.

Within equities, we added to sectors where the market weakness was more pronounced, such as financials and technology. Opportunities presented themselves in certain Magnificent 7 stocks where valuations became disconnected from the underlying moats of their businesses. For perspective, during the first quarter the Magnificent 7 ex-Tesla traded cheaper than the Consumer Staples sector4.

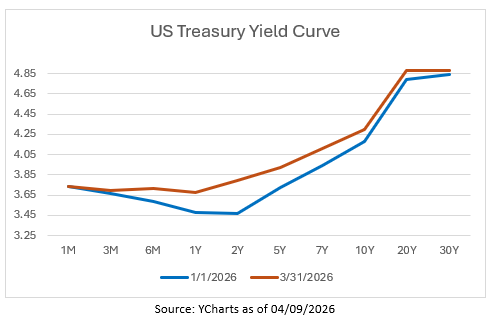

In fixed income, higher yields – particularly in intermediate maturities – have improved prospective returns going forward. The flattening of the yield curve given our positioning allows us to capture more attractive yields without taking on additional volatility that often accompanies extending duration.

Looking Ahead

We would expect more volatility in the months ahead, especially if ceasefire talks with Iran breakdown. However, we’re encouraged by the resilience of consumers and businesses to start the year.

Look no further than artificial intelligence (AI)—still the dominant market driver—as an example of the U.S. economy’s dynamism. AI is reshaping industries ranging from robotics and biotechnology to defense and beyond.

There are still open questions around the pace of investment and ultimate returns, but one thing is clear—AI adoption is accelerating. Companies that are embracing AI are already being rewarded, and over time we expect the benefits to extend broadly across industries through productivity gains, cost savings, and improved profitability.

Given the range of possible outcomes, we continue to emphasize diversification — balancing growth opportunities with more defensive holdings. This approach is designed to help portfolios navigate different environments while remaining positioned to participate in long-term upside.

Prices across equities and fixed income are more attractive today than just a few months ago—and staying the course during periods like this is often critical to long-term success.

Thank you for your continued confidence.

Bryce Goldbach, CFA®

Co-Chief Investment Officer

4/9/2026

Citations

[1] www.brainyquote.com Niels Bohr.

[2] www.strategas.com “Quarterly Review in Charts Wed. Apr 1, 2026.”

[3] www.strategas.com “Policy Outlook Thu. Apr 2, 2026.”

[4] www.chartkidmatt.com “The Craziest Stat of 2026.” Matt Cerminaro. 02/24/2026.

[5] www.ycharts.com “Treasury Yield Curve as of 04/09/2026.”

[6] www.yardeni.com “Sweet & Sour: Iran, China, M-PMI, & PPI.” Ed Yardeni. 03/03/2026.”

Disclosures

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Asio Capital makes no representation or warranty as to the accuracy or completeness of the information

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Asio Capital makes no representation or warranty as to the accuracy or completeness of the information

Disclosures

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Asio Capital makes no representation or warranty as to the accuracy or completeness of the information